As often as we hear the advice to keep our emotions out of investing, there’s no escaping the emotional impact of an election.

That’s true on several levels, including your investments. Even if you cheer the results (and I’m not about to take sides in this column – it’s a little late for that, in any event), you may feel a sense of trepidation about what the results mean for the markets.

In the short run, we know what it’s meant for U.S. stocks, which rallied to fresh highs. We also know that the bond market has shown its propensity to move in the opposite direction – with a vengeance!

But how can an investor stick to his or plan, over the long haul, regardless of news-driven movements in the equity and fixed-income markets? Remember Brexit? When the S&P 500 plunged 3.59% on June 24, only to rebound the following week and rally to new heights? Retail investors who bailed on the Brexit news were forced to buy back in at higher prices – if they returned to the market at all. Who knows? Some probably continued to sit it out and missed the post-election rally too.

One of the things I write about regularly is the importance of diversification, or including in your portfolio assets with low correlation to each other. For example, while the S&P 500 has been in rally mode since the election, global bond markets took a hit, with fixed-income investors nervous that President-elect Trump may increase government borrowing and spending.

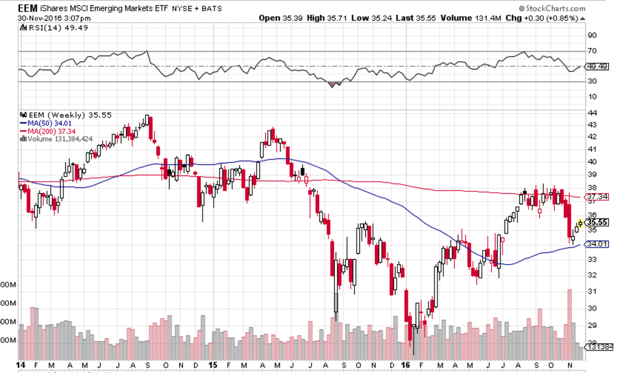

Meanwhile, emerging markets, which have been on a tear this year, are now skidding. The iShares MSCI Emerging Markets ETF (NYSEARCA:EEM) shed more than 4 percent in November, after rallying 6 percent between January and October. (However, it’s worth noting that the emerging market index staged a post-U.S.-election rally after being down more than 5 percent earlier in the month.)

Those two data points, alongside the S&P’s strong November performance, beg the question: What exactly do we mean when we say, “The market?”

Ask most American investors that question and they are likely to say “the S&P 500.” Anecdotally, I’ve observed that people over 70 often say “The Dow.”

Both answers are incorrect, or at least, incomplete.

The S&P 500, as a collection of the largest private stocks in the U.S. economy, gives you a very good sense of how domestic equities are doing. The S&P 500 companies comprise about 80 percent of the total U.S. market capitalization and about 42 percent of world market cap.

For the sake of discussion, let’s go ahead and call the S&P 500 “the market.” It’s not a bad surrogate, given its collective value.

A Market Of Stocks

To understand how the S&P 500 stocks might respond to an election, or any other important world event, it’s best to start by looking at the companies themselves. Sometimes, when tracking market movements, we overlook the obvious: When you invest in the market, you buy ownership of these companies. You’re buying ownership in giants such as Apple (NASDAQ:AAPL), Microsoft (NASDAQ:MSFT), Exxon Mobil (NYSE:XOM) and Johnson & Johnson (NYSE:JNJ).

In other words, the S&P 500 is not a monolith, but a collection of stocks. There’s a particularly inane phrase I hate, because it’s tossed around by stock pickers: “It’s not a stock market; it’s a market of stocks.” Turns out, there’s a kernel of truth, after all.

Obviously, the fate of the broader index is more tied to the largest companies, such as the ones named above, rather than First Solar (NASDAQ:FSLR) or Lamb Weston (NYSE:LW), some of the smallest components within the index.

When considering how “the market” might react to an election, a new presidential administration or any other event, drill down to the individual market components. There’s a tremendous amount of fear and uncertainty right now. That’s understandable; few predicted that this election would turn out the way it did.

But how do the companies themselves, as opposed to that amorphous blob known as “the market,” respond to major news events? To take an additional step back, ask yourself this very basic question: What exactly do you get when you buy a stock?

The answer is pretty obvious: ownership in a company. The value of what you own depends on the profits that the company will earn. When you buy a stock, you buy yourself a stream of profits, for as long as the company exists, or until you sell the stock, whichever comes first.

For example, if your great-great-grandparents bought shares of Standard Oil back in the 1880s, and the family managed to hang onto them all these years, the company now known as Exxon Mobil would have deposited a dividend into your piggy bank, for more than a century. Every single year. That’s a lot of profit going into investors’ pockets.

Even if you cringe when thinking about the profits of an oil company, consider other behemoths like Alphabet (NASDAQ:GOOGL) (NASDAQ:GOOG), Apple, Microsoft and Coca-Cola (NYSE:KO). Over the years, have their profits been significantly impacted by the occupant of 1600 Pennsylvania Avenue? History shows that the companies’ strategies, products and industry conditions matter more than who is in the White House.

That’s not to say it doesn’t matter who is president. It matters for one very important reason: Uncertainty. We’re at a crucial juncture now, just before a new president takes office and uncertainty is running high.

Uncertainty Is Always Certain

Year in and year out, a company’s profits are uncertain to begin with. That’s part of the risk when buying a stock or a bundle of stocks: You have no idea what the profits are going to be. Assuming markets are efficient, the price you pay today should reflect all the profits you expect to receive in the years ahead. That’s where the importance of a company’s products, its brand equity, its competitive landscape and management’s ability to execute on a strategy come into play.

But how does political uncertainty affect those factors? Through thick and thin, companies continue doing business. Apple is planning new iPhone releases. Tesla (NASDAQ:TSLA) is in the process of acquiring SolarCity (SCTY). Meanwhile, McDonald’s (NYSE:MCD) struggles with consumer eating habits that are changing dramatically, and companies including PepsiCo (NYSE:PEP), Kellogg (NYSE:K) and Mondelēz (NASDAQ:MDLZ) have cited Venezuela as a growing problem in their quarterly filings with the Securities Exchange Commission.

But what if a company believes a president’s policy on trade with China, for example, may affect its operations. Well, Apple reportedly is in discussions with vendors in its supply chain to produce certain products stateside, rather than in China. That is likely a result of concerns about President-elect Trump’s potential policies regarding foreign trade.

For the time being, there’s still uncertainty about what a Trump presidency may mean for the U.S. and its trading partners. When that uncertainty subsides, and it will, companies and their investors will heave a collective sigh of relief – not because they necessarily agree or disagree with the new president’s policies, but because they will know where things may be headed.

But there are always surprises that lurk. That’s just life.

The best recent example of this is Brexit. The day after the surprise election results in the U.K., the Morgan Stanley Capital International World Index, which tracks performance of large and mid-cap stocks across 23 developed markets, including the U.S., shed more than 5 percent. It bounced back the following week. As it became clear that the U.K. exit from the European Union would be a drawn-out affair, rather than a swift and chaotic breakup, the index rebounded. Since then, uncertainty about interest rates in the U.S. and Japan caused spikes of volatility. In other words, various events cause investor anxiety. The events pass, stocks tend to gravitate back to the mean, then another event comes along to worry investors and cause volatility. Wash, rinse, repeat.

Does all that market movement mean the companies in the MSCI World Index were not profitable, or that investors expected a sudden cessation of profits? Hardly.

Did it mean that those companies are not profitable anymore? That the value of those companies had suddenly plummeted to zero? Of course not. What it meant was that there was more uncertainty around those same profits, but when the first round of dust settled, global stocks came right back up. That happened over the course of a week, not months or years.

How long do you think it took the U.S. market, at least initially, to rebound after the election-night rout?

Two hours.

By the time Americans were able to determine some kind of post-election trade (those who are inclined to trade on news events, in any case), it was likely too late.

To put it bluntly: Yes, an election is an incredibly important event, but it shouldn’t play a role in any kind of decision to shuffle around your portfolio holdings.

So what about concerns specific to potential policies of a President Trump? For example, the risk of the U.S. becoming more isolated, which could have an effect on profits of companies that source and sell their wares globally.

The likely scenario, which will get lost in the blur of reporting about “the market,” is that institutions – who account for about 80 percent of equity ownership and trading activity – will evaluate companies and sectors on their own, rather than as a monolith. Some companies will benefit from new policies more than others. But as investors and traders are all jockeying for position within the broader market, in the short term, it’s not unusual to see sharp upside and downside price and volume spikes.

Three Strategies To Weather Volatility

Of course, the most important question on investors’ minds is how to protect themselves from the market movements and turmoil. Even though we know the spikes tend to be short-lived, they are no less frightening.

There are three basic strategies for protecting yourself against the ravages of market volatility.

The first and most conventional way is to rely on forecasts about how markets and companies will fare in the future. With that system, investors find themselves trying to get into the market before a rise, and get out before a decline.

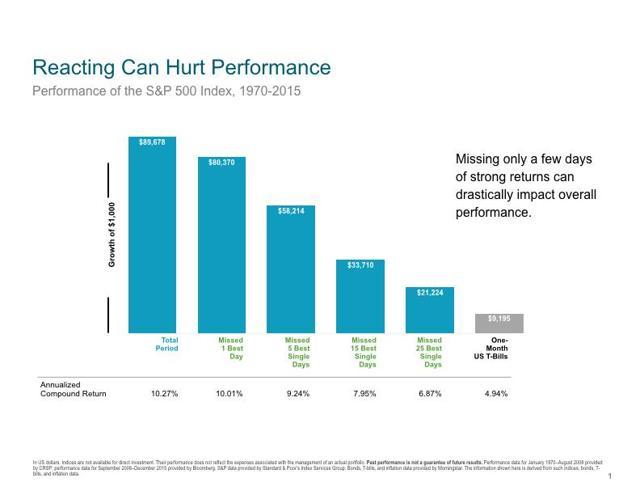

A large portion of the financial media is dedicated to the notion that you can trade in and out, in a timely fashion, to take advantage of market movements. Unfortunately for investors who attempt this strategy, Boston-based research firm Dalbar regularly publishes a report that shows the “average investor” fails to capture even the returns of the S&P 500 index, due to attempts at market timing, combined with trading costs. It’s tempting to try outwitting the broader market, but ultimately, it’s a fool’s errand.

To better understand why this trading methodology is difficult for individual investors to deploy successfully, let’s evaluate short- and long-term market behaviors.

Over the past several years, the S&P 500 has about a 55 percent chance of moving higher on any given day. Say you wake up one day and decide to put some money into the SPDR S&P 500 Trust ETF (NYSEARCA:SPY): You have a better chance of making money than losing. But it’s still essentially a crapshoot.

Source: Dimensional Fund Advisors

But what happens if you lose money that day and decide to bail out, and take a month off?

Well, over the course of a month, it turns out that the S&P 500 has a 63 percent chance of rising. So if you sit out for a month, you’re much more likely to miss out on gains. Sure, you protect yourself 37 percent of the time, but the odds are not in your favor.

On a yearly basis, your risk of incurring an opportunity cost increases when you sit on the sidelines. The S&P 500 has a 70 percent chance of gaining in any given year.

But does a one-year view really help when you are shepherding your assets for a goal like retirement? (That’s a rhetorical question, in case you didn’t catch that!)

When you look at five years, 87 percent of the time, you’re going to make money and 13 percent of the time you won’t. Of course, nobody can successfully guess at which days, months, years or five-year stretches will be fruitful and which won’t. That’s true regardless of how you think markets will respond to elections and other events.

The way to protect your capital is not by sitting it out, waiting for the proverbial second shoe to drop. The odds of you missing out on gains are significantly higher than the odds of escaping a loss.

Unfortunately, many in the financial media, along with peddlers of trading programs, would have you believe that skill, combined with the right way of analyzing the data, will lead you to the correct market-timing decisions.

You may know people who bailed out after Brexit, thinking the downturn was the catalyst for a prolonged correction. They said, “I’m done. I can’t take it. I had to get out.” About three months later, they were asking, “When should I get back in?” But they missed the recovery, which happened fast.

Fear is a pervasive emotion for investors. There are people right now, who got out in the bottom of ’08. Years later, they are still asking, “When do you get back in?”

So the way to protect yourself is not to be trading in and out of the market. As much as the world feels like it’s falling apart right now, it’s not the first or last time we’ll feel this way. One of the behavioral factors that can hurt investors is recency bias. Our brains trick us into thinking that what’s happened recently will continue to happen.

I wrote about that at length here.

But the companies that comprise indexes, such as the S&P 500 or the MSCI World Index, will continue to exist. Remember, in the “it all comes crashing down” imaginary scenario, all these companies cease to exist. If that happens, we’ll all have far more serious problems than we are discussing today.

Taking the “stay invested” discussion a step further, let’s look at the average return of the U.S. stock market. Over the past nine years, that’s been between 9 percent and 10 percent each year.

What Is Average?

So here’s a question for you: Since 1926, how many years has the S&P 500 returned between 9 and 10 percent? That’s the average, so it must have happened quite a few times, right?

Wrong.

The answer is zero. Goose egg. Nada.

That sounds weird, doesn’t it? The market has never returned its average. That means the average is masking a huge degree of choppiness. The markets go up 15 percent one year, and they lose 10 percent the next. But as we’ve seen, over time, they have more good-performing years than poor-performing years. That’s where you get the 9 percent to 10 percent per year average return.

Yes, the nature of the market is to fluctuate. At the beginning of the year people were panicked because the market was in decline. I recall thinking, “Really? Has that ever happened before? Why are you so panicked about it? This is the way that markets work.”

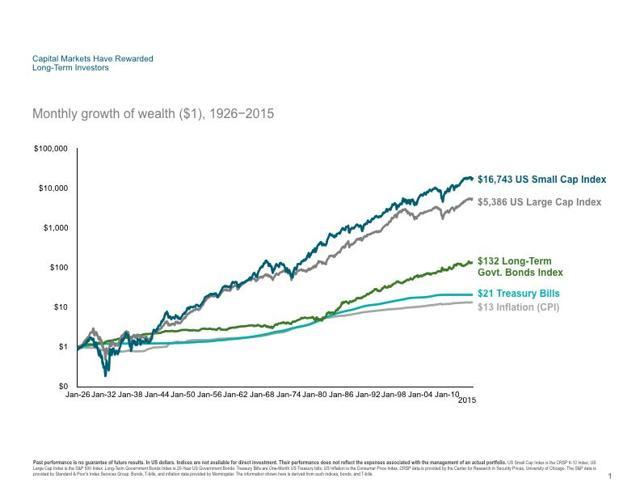

Say your grandparents or great-grandparents had invested $1 in the “Composite Index” in 1926. This was the precursor to the S&P 500. Assume that your ancestors kept their money in the Composite Index, even as it changed format a couple of times, eventually becoming the S&P 500 in 1957.

What would that $1 be worth today, if it had remained invested through all the recessions, the wars, the Great Depression, September 11 and many Presidential election cycles?

Today, it would be worth about $5,300. That’s nice growth, but it’s not steady growth! It takes some intestinal fortitude to hang in there, secure in the knowledge that no matter how horrible current events may seem, markets have overcome bad things before, and will again.

Of course, another way to protect yourself against sharp market fluctuations is by purchasing bonds.

Historically – and still today – a reliable fixed-income investment has been the 30-day U.S. Treasury bill. Sure, bond prices also fluctuate, but short-term, high-quality bonds tend to be less volatile. The trade-off for that reduced volatility is a lesser return; long-term bonds deliver a higher return because investors demand to be paid more for taking a greater risk. It’s less clear what interest rates will be 20 years from now. That’s why long-term bonds pay more but tend to fluctuate more.

Say that same ancestor who put $1 into the Composite Index in 1926 also decided to balance his portfolio somewhat, and invested another $1 into a U.S. Treasury bill. That investment is worth about $21 today.

Yes, that fixed-income investment stayed ahead of inflation. It also served as ballast during severe market downturns, such as 1974 and 2008.

Source: Dimensional Fund Advisors

But investors get impatient with bonds. For example, instead of earning 9 percent or 10 percent per year, your average annual return on a Treasury bill is more like 3 percent to 4 percent. It’s really a way of protecting a certain portion of your capital, rather than investing for growth.

In the past, retirees would often stash every penny into bonds. But these days, with more and more Americans living to 100, it’s crucial to have growth, not just the perception of safety that comes with bonds.

In truth, that “perception” is an old-school notion. Today, investors understand that bonds can also be volatile. Still, I continue to run across retirees who believe that because they are older, a portfolio stashed entirely in bonds is the best course. Maybe that was somewhat true when life expectancy was shorter, but that advice is less applicable with every passing year.

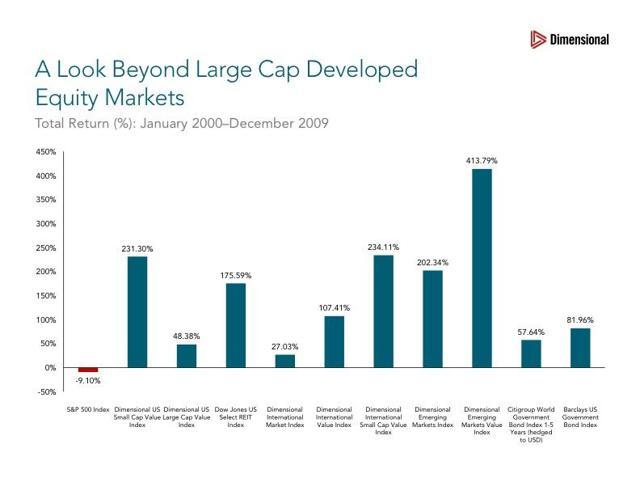

The second way to protect yourself against volatility is through basic geographic diversification. More often than not, there is a benefit to looking at opportunities, not only in the US, but across the world. U.S. stocks account for roughly half of the world’s total market capitalization. In this day and age, it’s not enough to ignore the rest of the world. The graphic below illustrates the time period from January 2000 through December 2009. While large U.S. stocks languished and analysts wrote about “getting back to even,” other global asset classes more than made up for the deficiencies of the S&P 500.

Source: Dimensional Fund Advisors

Investors who held a portfolio diversified by asset class and geography had no concern about “getting back to even.” They were already on track.

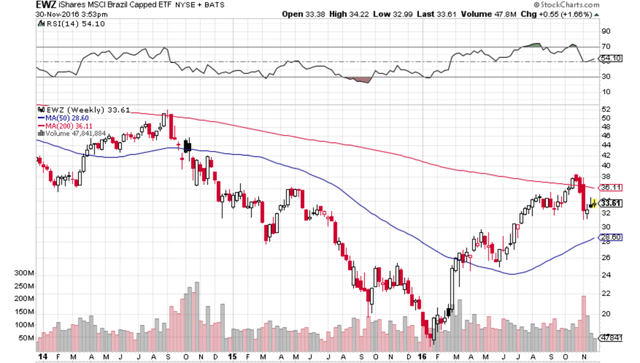

Here’s a good example of why it’s unwise to limit your investments to only U.S. securities: Over the past 30 years, the U.S. stock market has never been the best-performing global market. So far in 2016, the iShares MSCI Brazil Capped ETF (NYSEARCA:EWZ), which tracks the MSCI Brazil 25/50 Index, is up 63 percent.

When I give examples like that, sometimes the point is misunderstood. Sometimes people like to give a snarky little chuckle and say something like, “Who would invest in all Brazilian stocks?”

Sorry, snarkers. You missed the point completely. Nobody would have chosen Brazil as the best-performing global market. In 2015, the best-performing developed market was Denmark. It’s doubtful you would have decided to go all-in on Lego or Tuborg beer. Instead, you want to own stocks from Denmark, Brazil, the U.S. and all the other developed and emerging markets. That way, you capture the world’s best-performing markets in any given year.

Protect yourself from the uncertainty of the US. Buy some stocks abroad, preferably as part of a diversified basket, rather than trying to bet on single companies.

Finally – and this is huge – the third way to protect yourself from volatility is to understand the behavioral component to investing. Investors tend to make decisions that stem from emotions such as fear and greed. People don’t like hearing this, because they believe investing is purely logical and data-driven. Unfortunately, people tend to couch emotional decisions as being “logical.” They cite predictions from somebody or other on the internet as the basis for their logical decision.

If it were that easy, wouldn’t everybody just make the correct logical decisions year in and year out? Everybody would constantly be a winner in the market. Trophies for everyone.

We know it doesn’t work that way.

Traditionally, these emotions played out as investors panicked and sold out when stocks were falling, and became hopeful and snapped up shares as stocks were nearing a peak.

These days, depression about stocks has a “pre-emptive” quality to it. People tend to anticipate horrible things and bail out before they happen. Problem is that’s market timing and market timing doesn’t work.

Think about it: If we could accurately predict how markets would behave based on logical-sounding prognostications from our favorite economists or market “gurus,” investing would be easy. Magic formula!

In the old days, the role of a stockbroker was to pretend he knew something about what markets would do in the future. In Grandpa’s era, perhaps the brokers had access to research reports that the average investor didn’t have, but even those were not foolproof. They still aren’t, by the way.

But all of us have access to essentially the same information today. For those who continue to attempt market timing, remember: There’s somebody on the other side of your trade. So for all your belief that your prediction is “logical,” somebody holds the exact opposite belief. You can’t both be right.

There’s a quote that’s widely attributed to Warren Buffett: “Be fearful when others are greedy and greedy when others are fearful.” I’m not certain whether he actually said that, but the advice is sound.

But what really happens? When markets start declining, the urge is to bail out in order to protect yourself.

The process of buying low and selling high is pretty simple, and it’s something advisors and professional asset managers do all the time. It’s called rebalancing. Say your ideal allocation calls for 20 percent of your money to be invested in the S&P 500. But as large-cap U.S. stocks perform well, they grow to become 25 percent of your portfolio.

Meanwhile, another allocation, the Barclays Aggregate Bond index fund, has decreased from 20 percent to 15 percent.

What do you do? Snap up more S&P shares to catch momentum? Sell off your bond fund because it’s a loser?

Neither.

You rebalance by selling some of your S&P shares to get that allocation back to 20 percent and you buy some more of the bond fund to increase your stake to 20 percent.

Not easy, is it? It’s a little bit counterintuitive and requires that you override your feelings of hope and fear. That’s where an advisor can help with the behavioral aspects. That’s a large part of what today’s advisors do. It’s a very different function than Grandpa’s stockbroker performed.

Those are three things that you can do to protect yourself as an investor. Although I listed the behavioral component as the third item, it’s really the most important and permeates all your other investment decisions.

The investment world has changed. Contrary to what you might believe if you are caught in the modern era’s pervasive fog of malaise and gloom, investors have it better today than in the past. We can put the science of investing to work for us. That’s a whole lot better than relying on some guy to call you and say, “I’ve got a hot stock for you!”

And in case you are snickering because that’s so old school, consider this: Instead of waiting for that phone call, you’re turning to some internet pundit to give you the same guess.

Not very scientific, is it?